Homeowners sitting on a mountain of debt

Usually seen as prudent and cautious, the Swiss are currently among the most indebted homeowners in the world. The tax system and market conditions are fuelling the mortgage boom and the powers that be are starting to worry.

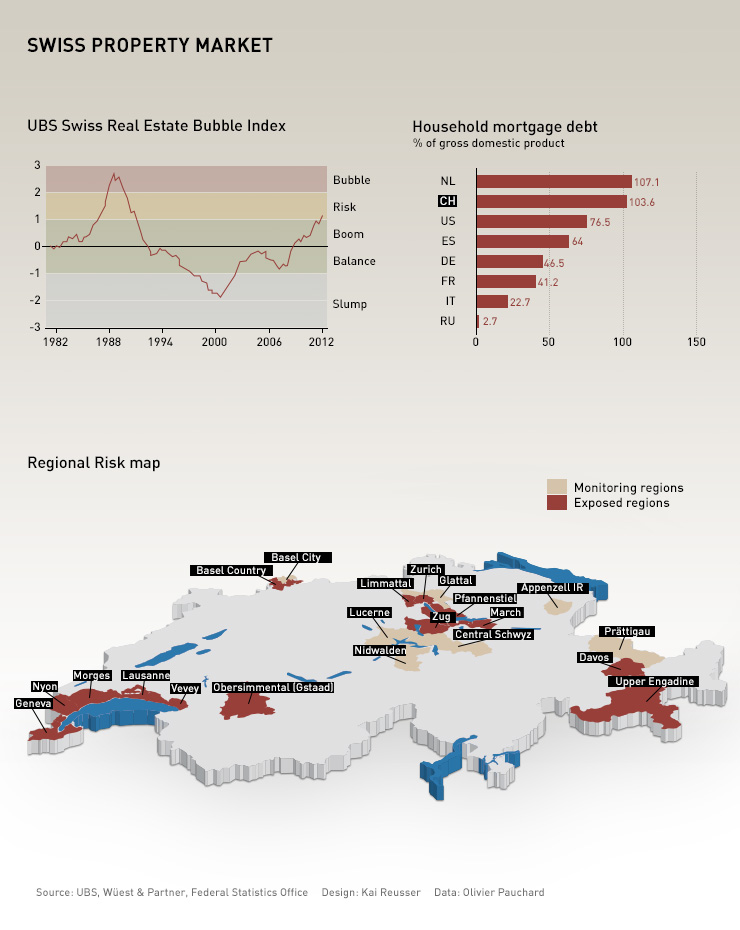

According to the Swiss National Bank, total mortgage credit reached a new high of SFr614,244 billion ($668,819 billion) last year, which represents 103.6 per cent of Switzerland’s Gross Domestic Product (GDP).

It’s almost a world record. Only the Netherlands has a higher rate, at 107.1 per cent. Among the countries with significant mortgage debt are the United States (76.5 per cent) and Spain (64 per cent).

A high level of indebtedness is not always a forerunner of a catastrophe, however. “The figures are certainly impressive,” said Philippe Thalmann, economics professor at Lausanne’s Federal Institute of Technology (EPFL) and a property market specialist. “The total sum of those mortgage debts represents a debt of around SFr250,000 per property. But this debt is less than half the average property value of SFr600,000. The prices would really have to fall by half for things to become worrying for most homeowners.”

More

Charting Swiss property highs and lows

Official worries

This doesn’t stop the ranking from causing concern. The Netherlands saw their property bubble burst last year, the US had the subprime crisis, and Spain is faced with a devastated property market. Switzerland is therefore not necessarily safe from unwelcome surprises, even though the current conditions – low interest rates, strong demand for apartments, buoyant economy – remain good.

The Swiss authorities are in any case conscious of the risks and are calling for prudence. In February 2012 the finance ministry’s Financial Stability working group wrote in a report on market surveillance:

“A high level of debt strongly exposes households to certain risks, such as a marked increase in interest rates. A fall in property prices accompanied by higher interest rates could destabilise the property market if the capacity of numerous households to support these debts is exceeded. Therefore any financial policies which encourage excessive debt of households should be avoided.”

In another document about the evolution of the Swiss property market and the role of the state, the finance ministry again warned that “a rapid increase in interest rates could produce critical situations. This is the case when a correction of property values occurs and a significant number of mortgage debtors find they suddenly have difficulty paying. The problems risk spreading to the banks and even the entire financial system. In the worst-case scenario this could require the costly intervention of the state.”

Other authorities – the Swiss National Bank, the cabinet and the Swiss Financial Markets Supervisory Authority (Finma) – have also expressed their concern more than once.

The Swiss government announced on February 13 that it was taking action to prevent excessive rises in property prices and high mortgage debts by forcing banks to rein in their lending.

At the request of the Swiss National Bank (SNB) , the government has decided that as of September 30 banks will be obliged to hold an extra one per cent in capital reserves to cover the risk of mortgage loan defaults.

The measure would force banks to retain around an extra SFr3 billion ($3.3 billion) in capital reserves, thus restricting the amount of loans they could issue.

Low interest rates coupled with high rates of immigration have been blamed for the average property price rising by nearly a third within the last decade. In some “hotspot areas”, such as Geneva, prices have increased by an estimated 136 per cent.

The government could order banks to set aside a maximum of 2.5% extra capital to cover mortgage risk.

(Updated on February 13, 2013)

System flaws

The indebtedness of households has increased in recent years mainly because of historically low interest rates. These are so low – currently between 2% and 2.5% for a 10-year fixed-rate mortgage – that homeowners don’t hesitate to go deeper into debt in order to buy property whose value keeps rising.

But the system is also skewing the market. Contrary to most other countries, it is not necessary in Switzerland to pay back the borrowed capital, even after a long period. Internal bank directives only require that a third of the debt be paid off within 20 years or when retirement age is reached.

“In Switzerland, banks do not require the clearing of mortgage debt, while in France or Italy, it has to be paid back in 20 or 30 years,” Thalmann explained. “On the contrary, banks are very happy when they are not paid back, because that is a relatively lucrative market for them.”

Mortgage rates have not been this low since 1850.

When calculating the cost of a mortgage loan, banks take a historic average of five per cent.

Currently, the rate for a 10-year fixed rate mortgage is between two per cent and 2.5 per cent. For shorter-term loans or variable-rate mortgages the rate can be as low as one per cent.

There is, however, a perverse effect, because low interest rates have the effect of pushing up property prices.

Rental value

The Swiss tax system has another peculiarity which encourages debt. In most cantons, owners who occupy their property have to pay tax on the theoretical rental value of their property, as if they were actually receiving that income.

“From the point of view of fiscal theory, the imposition of the rental value tax is a good measure. It provides equality of treatment between the homeowner who uses his or her accommodation and those who rent it out. In effect the owner-landlord who receives rent has to declare that income to the tax authorities,” Thalmann explained.

On one side of the balance sheet, the homeowner who lives in his property has the fictitious rental income added to his or her taxable income. On the other side the taxpayer can include as deductible expenses mortgage interest payments and any expenditures going toward the upkeep of the property. From a tax point of view the owner occupier therefore has an interest in keeping the debt and the interest attached to it.

To limit the risks, the authorities have already urged the banks to reinforce their self-regulation measures in granting mortgage loans. New rules have been in place since July 2012.

Reforming these tax incentives would be one way to put the brake on debt, but previous efforts to do so have come up against popular resistance. “The efforts with a view to reforming the taxation of property did not bear fruit in the past. In the past 13 years, three proposals were rejected at the ballot box, all of which proposed different modifications to the rental value tax,” a recent cabinet statement said.

(Translated from French by Clare O’Dea)

In compliance with the JTI standards

More: SWI swissinfo.ch certified by the Journalism Trust Initiative

You can find an overview of ongoing debates with our journalists here . Please join us!

If you want to start a conversation about a topic raised in this article or want to report factual errors, email us at english@swissinfo.ch.