Could Switzerland be facing a property bubble?

There are signs of a property bubble in Switzerland, according to recent studies, but other observers say the situation should remain under control. To be on the safe side, the authorities have called on the banks to tread carefully.

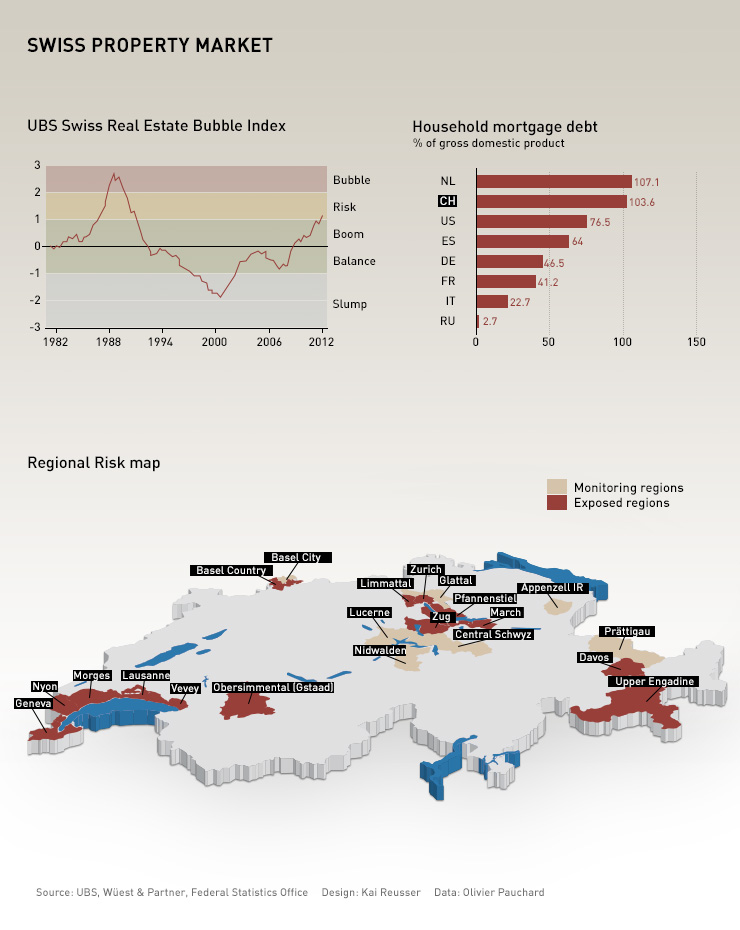

A study published by the UBS bank earlier this month said the risk of the market overheating, already present in the third quarter of 2012, increased in the fourth. “The index lies clearly in the risk zone, confirming the increased imbalances in the real estate market,” it says.

A study conducted by the price comparison site comparis.ch and the Federal Institute of Technology of Zurich also sounded alarm bells: “Eleven districts are clearly tending towards a property bubble,” it says.

The places most at risk are big urban areas like Geneva and Zurich and their immediate neighbourhoods, as well as some popular tourist resorts.

“There’s been a clear slow-down since last summer,” François Hiltbrand, of the Geneva-based firm Analyses & Développements Immobiliers (Property Analysis and Development), told swissinfo.ch. “We are seeing the number of sales going down, while the prices remain high. This shows that we are in a bubble.”

The Swiss government announced on February 13 that it was taking action to prevent excessive rises in property prices and high mortgage debts by forcing banks to rein in their lending.

At the request of the Swiss National Bank (SNB) , the government has decided that as of September 30 banks will be obliged to hold an extra one per cent in capital reserves to cover the risk of mortgage loan defaults.

The measure would force banks to retain around an extra SFr3 billion ($3.3 billion) in capital reserves, thus restricting the amount of loans they could issue.

Low interest rates coupled with high rates of immigration have been blamed for the average property price rising by nearly a third within the last decade. In some “hotspot areas”, such as Geneva, prices have increased by an estimated 136 per cent.

The government could order banks to set aside a maximum of 2.5 per cent extra capital to cover mortgage risk.

(Updated on February 13, 2013)

Rocketing prices

Property prices have shot up. Experts say they have increased on average by about 30 per cent in the past ten years. The increase has been much greater in the major cities, with Geneva holding the record: according to the analysts Wüest & Partner, prices there went up by about 136 per cent. And the UBS study says this is continuing: the price of accommodations rose by 1.2 per cent in the last quarter of 2012 in comparison with the one before.

But although prices have rocketed, this hasn’t slowed down construction, which has been encouraged by rock-bottom mortgage rates. Since it costs so little to borrow, more households now have access to the property market.

“Pure fables”

A bubble appears when the rise in property prices is out of kilter with other economic indices, such as salaries. The buildings eventually end up overvalued in terms of the real market. At a certain point the difference becomes too great, and the bubble bursts, dragging prices down. Given the current level of prices in Switzerland, experts are now talking about a bubble.

But not everyone agrees. In an interview with the German-language newspaper Tages-Anzeiger, Migros Bank head Harald Nedwed called the rumours of a bubble “pure fables”. The Swiss Bankers Association (SBA) is also optimistic. “Even if it can’t be denied that locally there are some signs of potential overheating, a generalised property bubble in Switzerland as a whole is not on the cards,” they said.

These differences of opinion are not surprising, given that it is not easy to identify a bubble.

“The problem is that while we can see a large rise in prices, there are good reasons for it: continued demand because the population is increasing, household incomes are stable or rising, and there is a relative shortage of accommodations. You can’t automatically talk about a bubble the minute prices start to take off,” explained Philippe Thalmann, professor at the Federal Institute of Technology in Lausanne and a property market specialist.

“As long as there is someone willing to buy these properties at these prices, we have to believe there is a demand. We can’t talk of unrealistic prices. But these are only possible as long as interest rates remain very low, demand stays strong and the economy is stable.”

More

Charting Swiss property highs and lows

Self-regulation

However, the upsurge in prices and the increasing indebtedness of households has led the Swiss Financial Markets Supervisory Authority (Finma), the finance ministry and the Swiss National Bank (SNB) to call on banks to be careful about making loans.

The SBA has toughened its internal directives over mortgage lending. In June last year it suggested two new requirements: borrowers should provide ten per cent of the financing from their own resources, and not by taking it from their pension funds, and they should pay off a third of the debt during the first 20 years. These proposals were accepted by Finma and the government, and came into force on July 1, 2012.

These measures came on top of others introduced during the property crisis of the late 1990s. That was when buyers first had to start providing 20 per cent of the capital to buy property. The SBA has welcomed the fact that the government accepted these “complementary additional measures” as part of a system of self-regulation which has “proved its worth”.

But this self-regulation has its limits, since the banks have the possibility of making exceptions to their internal rules. They may lift the requirement for a 20 per cent contribution, or use too low a base interest rate to calculate the charges, or set a lower amortisation rate.

“We have observed that more and more exceptions are being made,” Finma spokesman Tobias Lux told swissinfo.ch. “They are permitted, but if there are too many, we want to know the reason, and above all know how the risks have been measured. We are following the situation very closely. If need be we can intervene with a bank and insist that it increases its own capital, in order to better cover the risks.”

Lessons learned

According to most experts, the situation should remain under control. They think the property market is much more likely to stabilise than to collapse. Indeed, the overall situation is still healthy: the SNB’s monetary policy in support of the franc against the euro makes it unlikely that there will be a sudden rise in interest rates, the high level of immigration is stimulating the demand for accommodations, and Switzerland seems still to be escaping the economic slump.

Even if interest rates were to rise, the consequences would be limited.

Hiltbrand is upbeat: “Given that the banks have been quite restrictive for several years now, it’s unlikely that people will find themselves in dire straits.”

“There will be no repetition of the mistakes of the late 1980s, when banks were lending more than 100 per cent to households that could offer practically no guarantees,” said Thalmann. “We had our subprime crisis at the beginning of the 1990s and the lessons were learned.”

A property market outlook for 2013 carried out by the research and consultancy firm Fahrländer Partner of Zurich indicates that prices in the luxury segment are falling and many properties aren’t selling as easily.

In general, the luxury market is regarded as properties whose price is at least 40% higher than the average price of a property in the area. Other criteria, such as an exceptional location or extremely high-quality fittings, are also included.

This segment is dropping in large part due to the financial difficulties being experienced by some wealthy Europeans.

“In Crans-Montana, where there are a lot of Italian clients, Italy’s current economic problems are having a major impact,” says Eric Nydegger of Projet Invest.

François Hiltbrand of Analyse & Développements Immobiliers says Switzerland is no longer as attractive as it used to be.

“With the gradual disappearance of tax packages and banking secrecy, rich clients are less and less inclined to settle in Switzerland,” he explains.

Philippe Thalmann, economics professor at the Federal Institute of Technology in Lausanne, suggests a third reason.

“There are a lot of promoters who wanted to enter the luxury segment because that’s where the greatest profits are to be made. There is over-supply when everyone wants to work in this segment, even in areas where it is perhaps not suitable,” he says.

(Translated from French by Julia Slater)

In compliance with the JTI standards

More: SWI swissinfo.ch certified by the Journalism Trust Initiative

You can find an overview of ongoing debates with our journalists here . Please join us!

If you want to start a conversation about a topic raised in this article or want to report factual errors, email us at english@swissinfo.ch.